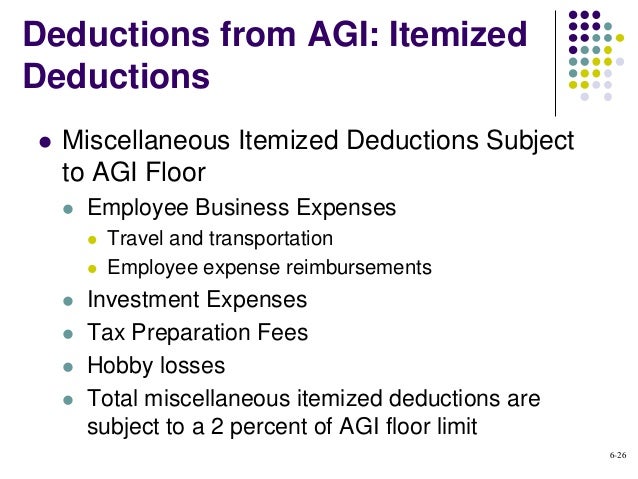

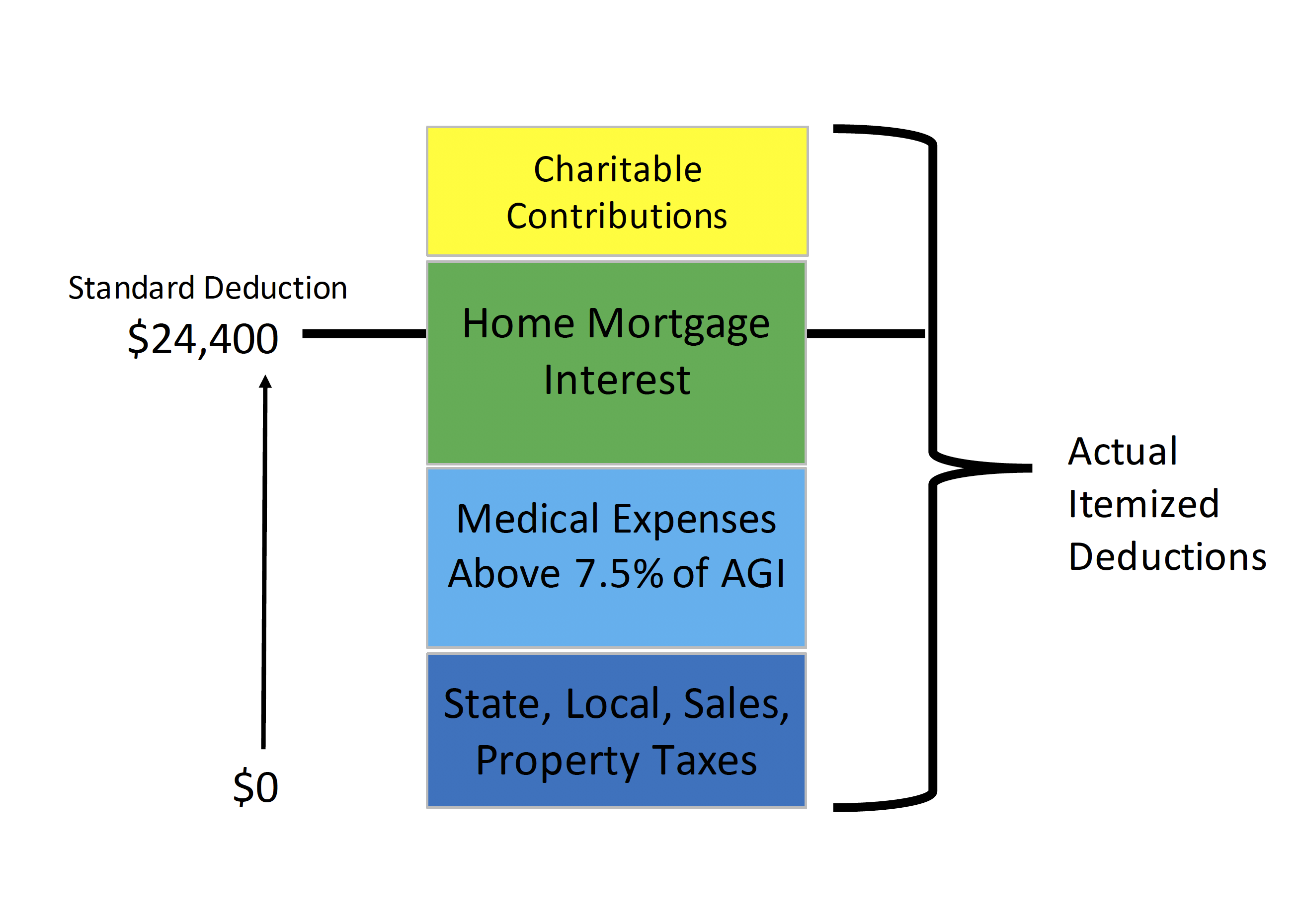

Subject To 2 Agi Floor

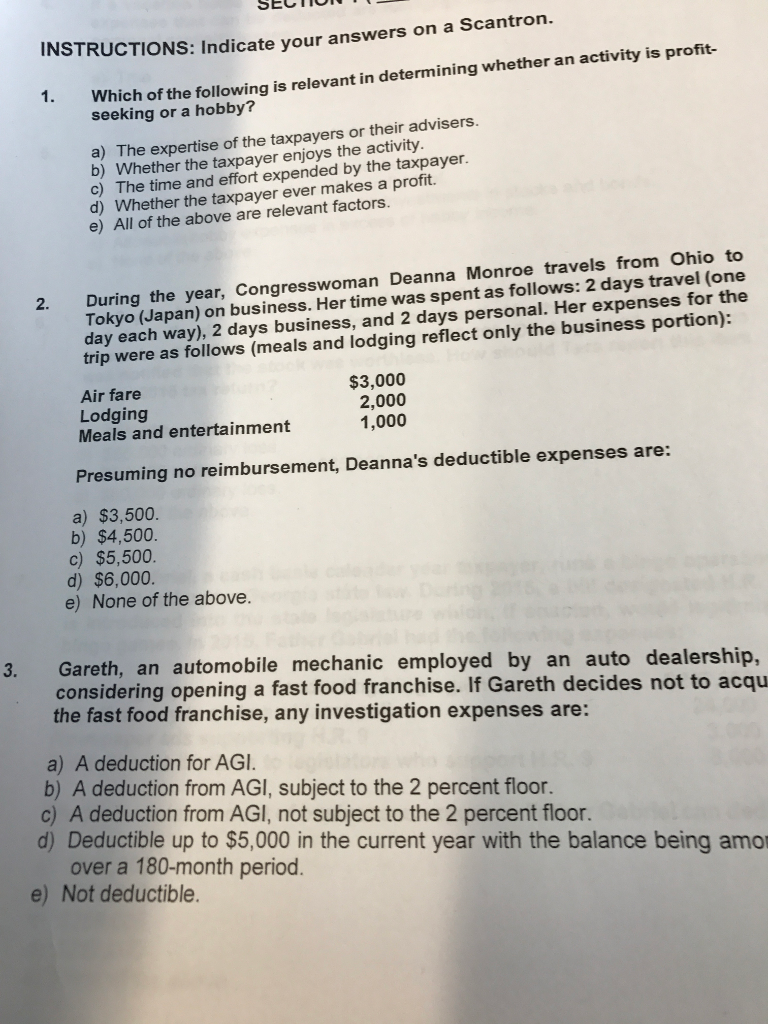

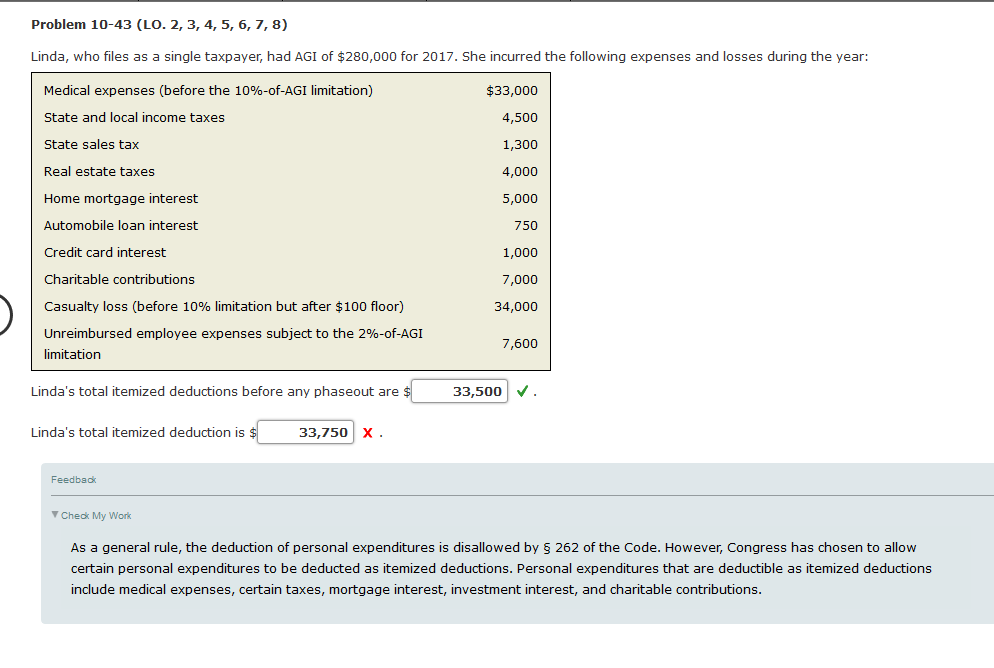

Solved Problem 10 43 Lo 2 3 4 5 6 7 8 Linda Who Chegg Com

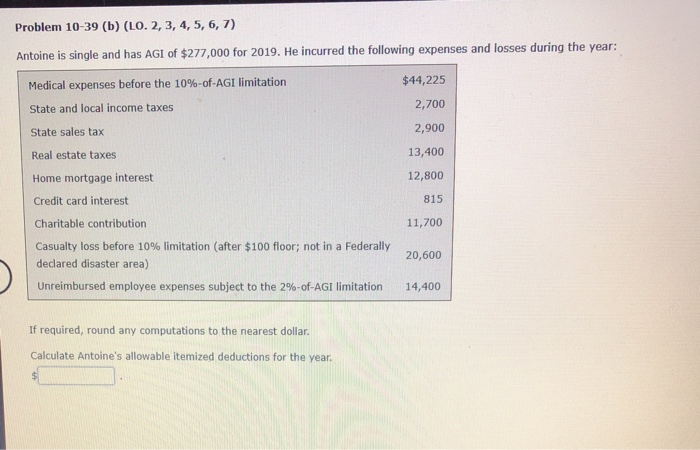

Solved Problem 10 39 B Lo 2 3 4 5 6 7 Antoine I Chegg Com

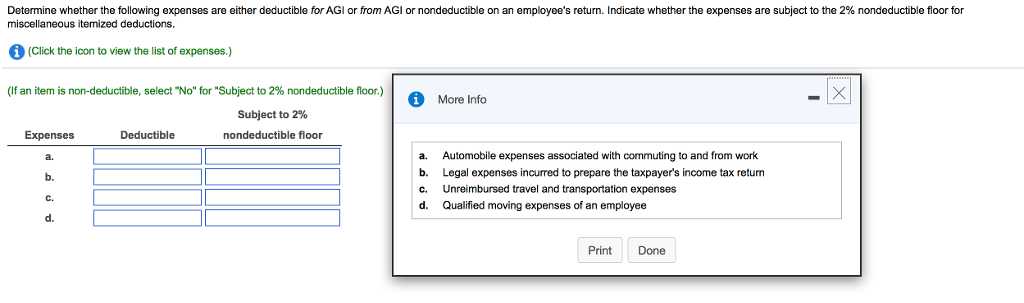

Solved Determine Whether The Following Expenses Are Eithe Chegg Com

Acct321 Chapter 06

March 2019 Charitable Contributions Are They Still Tax Deductible Marin Financial Advisors

Job hunting expenses for a position in the same trade or business.

Subject to 2 agi floor. His miscellaneous itemized deductions total 2 000. The following are itemized deductions subject in total to the 2 rule described above. For 1987 a a member of congress has adjusted gross income of 100 000 and miscellaneous itemized deductions of 10 750 of which 3 750 is for meals 3 000 is for other living expenses and 4 000 is for other miscellaneous itemized deductions none of which is subject to any percentage limitations other than the 2 percent floor of section 67. 1 year delay in treatment of publicly offered regulated investment companies under 2 percent floor pub.

Expenses for uniforms and special clothing. These include the following deductions. You can still claim certain expenses as itemized deductions on schedule a form 1040 1040 sr or 1040 nr or as an adjustment to income on form 1040 or 1040 sr. 2 000 1 500 2 of 75 000.

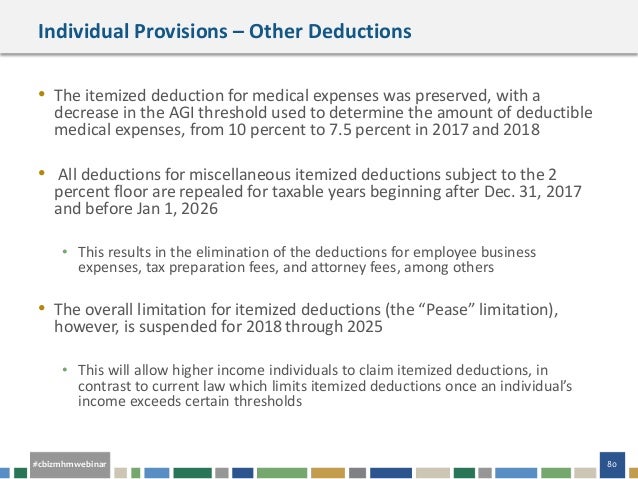

All products subject to id verification. The 2 rule referred to the limitation on certain miscellaneous itemized deductions which included things like unreimbursed job expenses tax prep investment advisory fees and safe deposit box rentals. Promotional period 11 14 2019 1 10 2020. Specifically the tcja suspended for 2018 through 2025 a large group of deductions lumped together in a category called miscellaneous itemized deductions that were deductible to the extent they exceeded 2 of a taxpayer s adjusted gross income.

In 2017 and earlier tax years wage earners and other taxpayers who weren t able to write thes. The amount of a s business meal expenses. 1330 386 provided that. If approved for an emerald advance your credit limit could be between 350 1000.

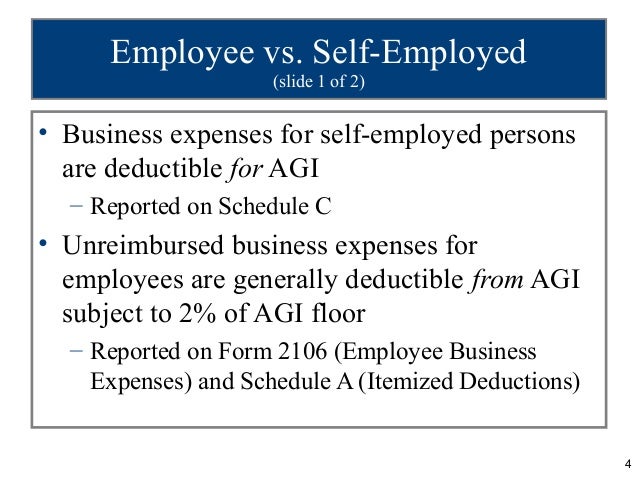

Line of credit subject to credit and underwriting approval. Products offered only at participating offices. These are work related. Unreimbursed employee business expenses such as.

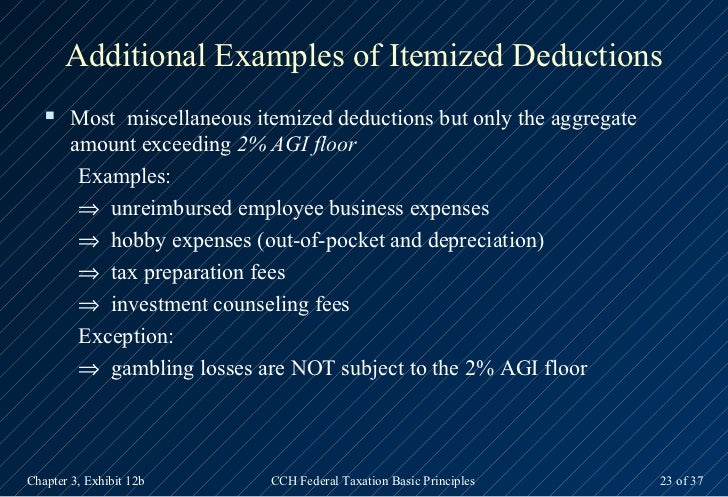

What are miscellaneous itemized deductions. Miscellaneous itemized deductions are those deductions that would have been subject to the 2 of adjusted gross income limitation. If he itemizes his deductions he can claim a 500 deduction for his miscellaneous items. Under knight fees paid to an investment adviser by a nongrantor trust or estate are generally miscellaneous itemized deductions subject to a floor of 2 of adjusted gross income agi rather than fully deductible as an expense of administering an estate or trust under sec.

Deductible expenses subject to the 2 floor includes. 1150 600 550 line 26 of schedule a even though he had expenses totaling 1150 because these particular expenses were subject to the 2 rule his net deduction that he will receive on his return for these expenditures is only 550. The supreme court held that the latter provision limits its. This publication covers the following topics.

Jerry s agi is 75 000. Work related education expenses to maintain or improve skills required for the position or to meet the demands of the employer.

Fernando Medina Poster For Neocon 22 Chicago 1990 Merchandise Mart Chicago Design Memphis Design

Object Fakir Chair By Agi Architects Chair Design Wooden Chair Artistic Furniture

Potential Tax Benefits With Images Disabled Children Williams Syndrome Parenting

Hi Everyone Meet This Week S Winner Of Gallerywallhashtag Soozi Soozidanson And Her Stunningly Eclectic Aesthetic Room Decor Retro Home Office Gallery Wall

Lush Agi Graphic Design Posters Japanese Graphic Design Graphic Design

Best Animation Institute In Jalandhar Animation Institute Cool Animations Learn Animation

2019 Ignant Norm Architects Architect Minimalism Interior

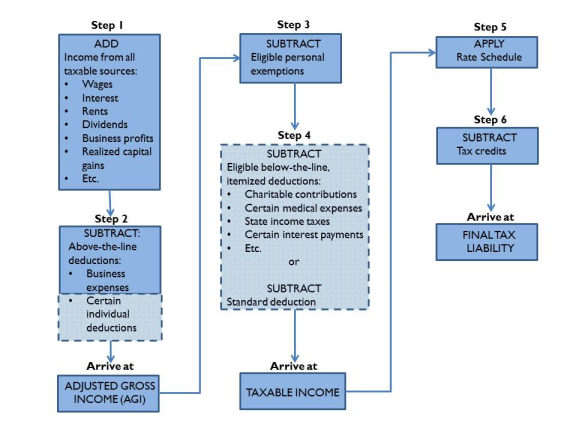

Tax Deductions For Individuals A Summary Everycrsreport Com

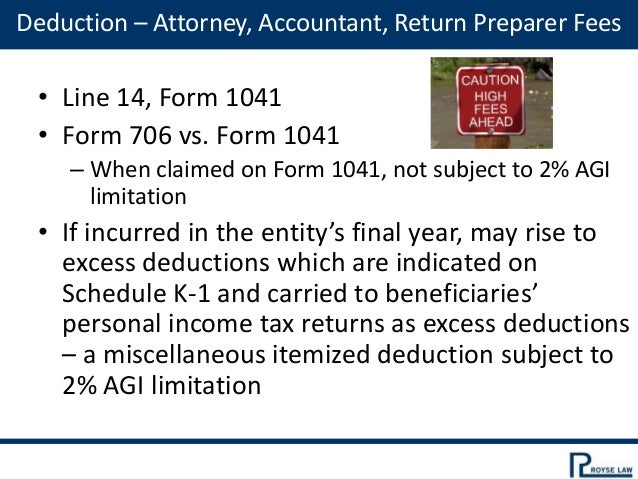

Https Www Drakesoftware Com Sharedassets Manuals 2017 Fiduciaries Pdf

Agi Student Show Klasse Wagenbreth Comics Artist Illustration How To Draw Hands

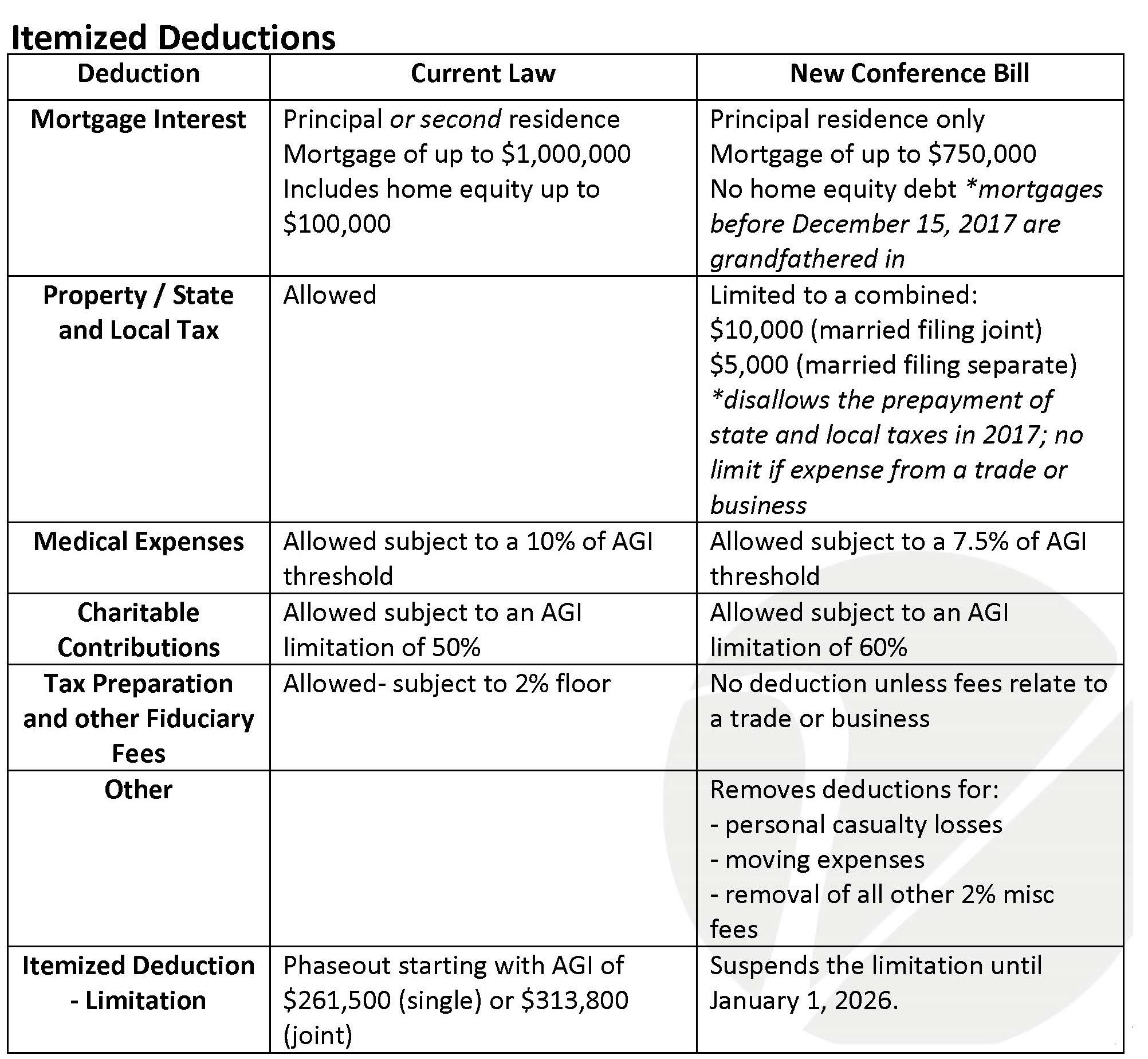

Tax Reform At A Glance How Does It Affect You

Cfp Income Tax Planning Flashcards Quizlet

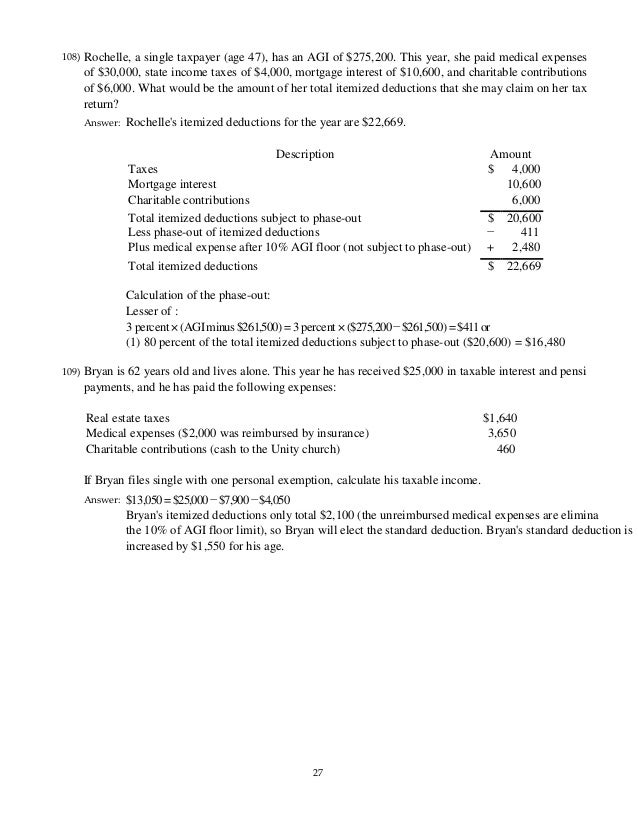

10 Archie Can Claim Total Deductible Medical Expenses That Exceed 7 5 Of His Adjusted Gross Income A True B False Homeworklib

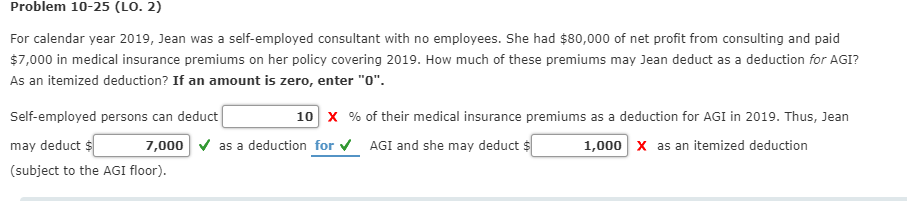

Solved Problem 10 25 Lo 2 For Calendar Year 2019 Jean Chegg Com

Taxation Of Individuals And Business Entities 2018 Edition 9th Editio

Object Fakir Chair By Agi Architects Geometric Furniture Chair Chair Design

Prestress Cross Sections Sabah Shawkat Structural Analysis Construction Drawings Engineering

Ppt Cch Federal Taxation Basic Principles Chapter 3 Individual Taxation An Overview Powerpoint Presentation Id 456975

Best Clat Coaching Institute In Jalandhar Coaching Mock Test Teaching

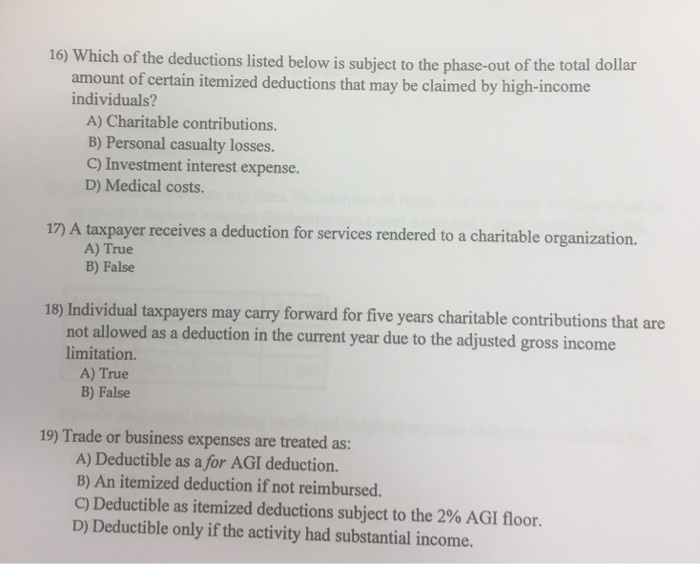

Solved Which Of The Deductions Listed Below Is Subject To Chegg Com

Daring Monochromatic Interior Scheme Home In Black Serenity In Taipei Dark Interiors Make Design Monochrome Interior

Https F01 Justanswer Com Pb4iwyno Multiple Choice Questions Pdf

Ppt Ch 09

Https Lawpracticecle Com Wp Content Uploads 2019 01 Lawpracticecle The New Tax Cuts And Jobs Act Pdf

Account Suspended Photography Studio Setup Studio Setup Studio Photography

Nab Docklands 2 700 Bourke Street Signage Design By Pidgeon Signage Design Wayfinding Design Floor Signage

Webinar Slides Tax Reform Is Here A Comprehensive Analysis Of The

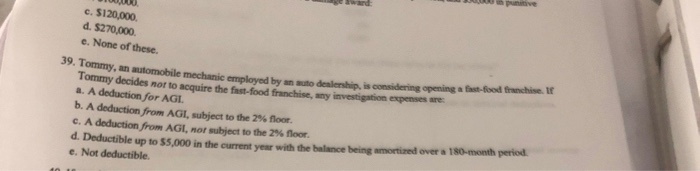

Solved C 120 000 D 270 000 E None Of These 39 To Chegg Com

Operating Theatre Design Google Search Hospital Design Architecture Hospital Design Healthcare Interior Design

Think Tax Reform Won T Impact Your Business Think Again Ppt Download

Graphic Designing Coaching Institute In Jalandhar Graphic Design Coaching Graphic

What S Going To Save You From The Mid Year Tax Changes C Suite Network Advisors

Pros And Cons Of Coffee Consumption Infographic Coffee Health Coffee Infographic Coffee Pros And Cons

2013 Cch Basic Principles Ch03

Free Download Floor Generator 3dsmax Script Cgramp Script Generation Flooring

Deductions And Losses Certain Itemized Deductions Ppt Download

See The World Education Poster Design Travel Poster Design Travel Advertising Design

Pin En 6 Bed 3 Bath Villa

Navigating Tax Reform For Manufacturers And Owners Ppt Download

New Study Argues Against Climate Change As Factor In Development Of Abyssal Hills Climate Change Climates Teaching Humor

Hort Hortberlin Fotos E Videos Do Instagram Visual Identity Poster Layout Environmental Design

Personal Development Plan Childcare Example Beautiful Personal Development Planning Help Your Drea Personal Development Plan How To Plan Personal Development

Federal Fiduciary Income Tax Workshop